Tokenomics analysis: Uniswap (UNI)

A DeFi platform - Decentralized automated market making swap exchange

Index

1. Introduction

This article intends to present Uniswap's key features and tokenomics by providing quantitative and qualitative insights to better evaluate the project for academic/research purposes. At the bottom of the article, you can find helpful links to deepen project knowledge.

This is not financial advice; always DYOR.

Uniswap (UNI) is the first Decentralized Exchange (DEX) built on the Ethereum network, implementing an automated market-making system (AMM) rather than a traditional order book. The DeFi protocol (Dapp) was launched in November 2018 by Hayden Adams, and many contributors have joined so far (Ethereum Foundation included). In 2020, it introduced a governance utility token (capital token) $UNI (fungible token) to give users (mainly Liquidity Providers) more incentive to utilize the protocol. It’s also worth mentioning the difference between a coin and a token.

Instead of matching individual buy and sell orders, users can pool together two assets that are then traded against, with the price determined based on the ratio between the two. Uniswap solves liquidity issues through decentralized automated solutions, allowing users to swap tokens with the minimum slippage and improving efficiency.

Users aren't required to deposit their funds or go through the know-your-customer process (KYC).

At the time of writing, Uniswap counts around $3.9 billion in Total Value Locked (TVL), fourth in the DeFiLlama TVL ranking list.

2. Key scores

Before going forward with the analysis, here you can find a summary of key metrics to evaluate the project's health quickly. Keep in mind that, except for grey and red ones, these scores are subject to my evaluation.

*It was recently discovered that one of the main holders of $UNI, the venture capital fund a16z, actually controls a great portion of voting power. This could lead to a protocol decentralization concern. View the related article to understand what is happened.

3. Protocol

a. Evolution

Initially, Uniswap didn’t have a proprietary token. However, in September 2020, SushiSwap launched its protocol starting from the original concept of Uniswap (since it is an open-source protocol) and added $SUSHI rewards to LPs. So, Uniswap went a step further: it became a DAO, creating its governance token ($UNI) to dampen the Vampire attack conducted by its rival. Since then, the liquidity providers of the protocol were also retrospectively rewarded with extra $UNI tokens.

So far, the first Uniswap version (V1) allowed several people to provide liquidity as well as create token pairs (pools). The main focus was to conclude smart contracts code, offer a user-friendly interface, and thoroughly audit SCs. Only ETH trading pairs were available at that time.

In May 2020, the second version of Uniswap (V2) launched, allowing direct swaps among ERC-20 tokens and reducing gas fees. Uniswap V2 offers LPs one fee tier: 0.30% on all trades.

In May 2021, the third Uniswap version was released (V3) with a more flexible and efficient AMM, letting LPs choose the price range they want to provide liquidity and accrue fees only within this range. V3 also reduces the issue of bad actors listing scam tokens on the platform. Uniswap V3 offers three tiers: 0.05%, 0.3%, and 1.0%.

Uniswap supports different EVM-compatible networks, other than Ethereum layer 1 solution (recently added also Celo), Polygon, Arbitrum, and Optimism as layer 2 protocols (layer1 vs layer2).

b. Protocol description

Unlike traditional order-book-based methodology, where users place limit orders and have to wait until they are fulfilled, by leveraging smart contract (SC) technology, AMM allows transacting automatically without relying on third parties to make the trades.

The AMM model takes advantage of liquidity pools representing crypto token pairs (e.g. ETH/USDC) locked in a smart contract. An algorithm makes trading possible by automatically setting token prices based on the supplied token ratio. Individuals provide liquidity to the DEX by adding a pair of tokens to a smart contract which can be bought and sold by other users according to the constant-product rule:

=xy}")

Liquidity Providers (LPs), or market makers, supply liquidity to pools and, in turn, are rewarded with trading fees charged to the trader, proportional to the liquidity provided.

There are tens of active pools within the ecosystem, making Uniswap one of the most liquid protocols of the entire crypto market, allowing users to trade with meager fees and slippage.

c. Value proposition

Uniswap’s product value proposition resides in an auto-routing system that automatically selects the best liquidity pools for swapping. The router splits individual trades across different pools to decrease gas costs, and an automated fee optimization mechanism lets users make transactions straightforwardly, minimizing the risk of failed transactions.

Below there is a demand-risk schema to understand the unique selling proposition (USP) and what factors could affect it:

In 2021, a study estimated that around half of all liquidity providers on Uniswap lose money through impermanent losses (IL). This happens because the revenue of 0.3% generated by trading fees is often less than the value lost through the price fluctuation of assets. Meaning that only certain liquidity pools are profitable in the long run.

Source: Soocial

d. Benchmark

Uniswap’s biggest rival is PancakeSwap, as it offers similar services. PancakeSwap leverages the BNB Smart Chain, allowing users to conduct network operations with lower gas fees than the Ethereum chain (e.g. Uniswap). PancakeSwap has built a highly gamified platform with lotteries, games, and contests to drive higher user engagement. But because Uniswap leverages the ERC-20 standard, it supports several token pairs and, in turn, has higher trade volumes than its BNB rival. Uniswap has a cleaner user interface with well-defined components that are easy to interact with. In contrast, PancakeSwap’s UI looks messier and more confusing.

Another relevant player is Curve which is, instead, focused on stablecoin pairs (this minimizes the users’ risk of impermanent loss) and BTC trades on Ethereum with low slippage and high liquidity pools. Curve enhances liquidity mining and yield farming but has a notably different distribution mechanism compared to Uniswap (treasury vs. ecosystem allocation), so both have a different strategy and selling proposition. In addition, the more and the longer $CRV are locked, the lower the fees for other services within the platform will be.

Worth also mentioning that Uniswap doesn’t offer part of the trading fees to token holders, while the other protocols, e.g. Sushiswap, do. By locking $SUSHI, users earn $xSUSHI that can be deposited as collateral on DeFi protocols (e.g. AAVE) to borrow against. Such architecture incentivizes holding $SUSHI.

Below is a comparison table among main UNI competitors highlighting some of the common DeFi metrics.

You can look at the following article for more insights about UNI’s benchmark.

4. Supply metrics

As per UNI’s tokenomics, let’s first discuss the key metrics affecting the token's supply and then try to understand if UNI’s incentives are value-aligned with the product and help create a common wealth within the ecosystem.

Below are the main supply data and volumes generated so far:

a. Distribution

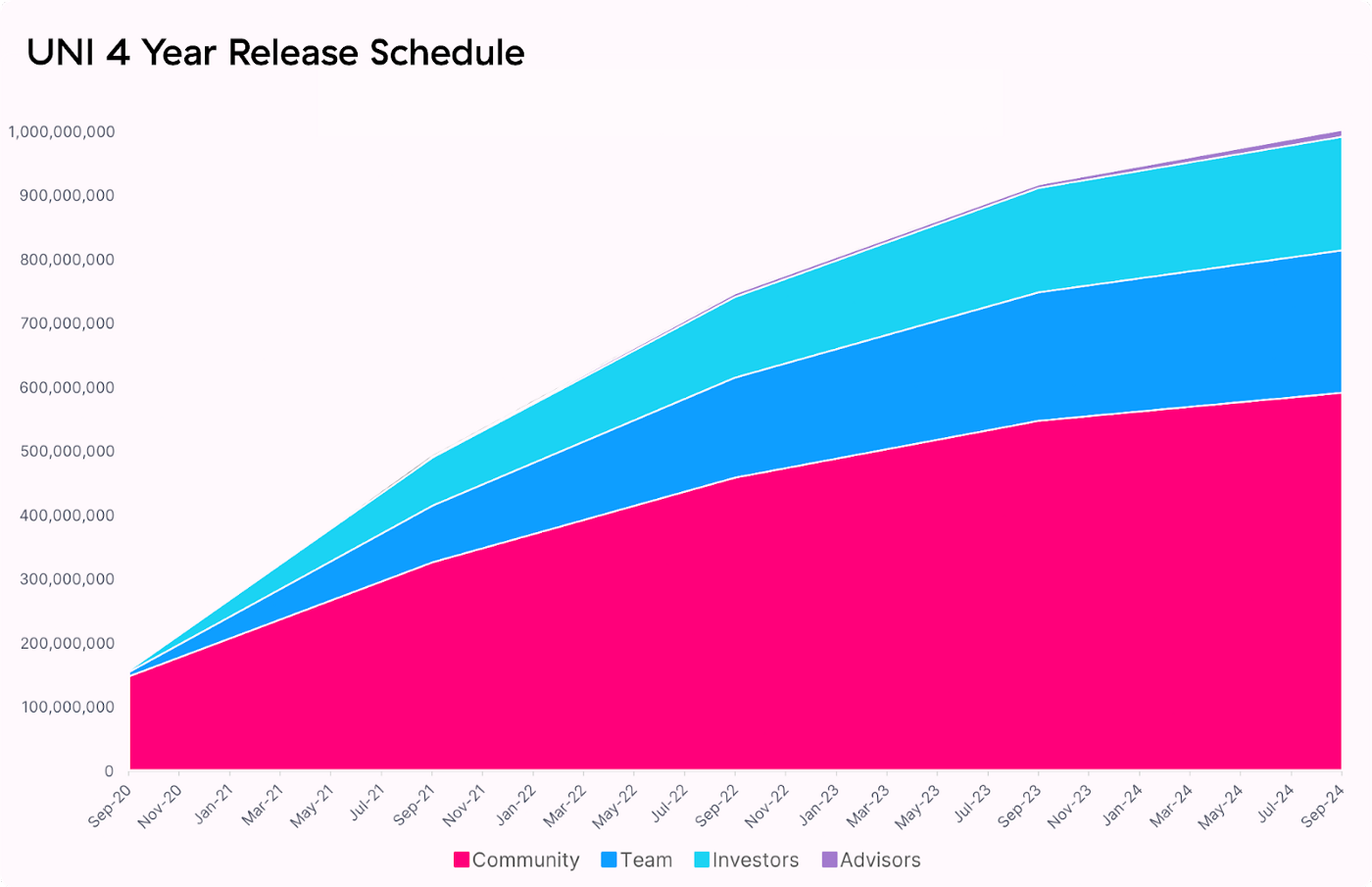

The initial four-year allocation is as follows (pre-mined token launch):

60% (600,000,000 $UNI) to Uniswap community members (treasury, ecosystem, and airdrop)

21.5% (212,660,000 $UNI) to team members with a 4-year vesting period

17.8% (180,440,000 $UNI) to investors with a 4-year vesting period

0.69% (6,900,000 $UNI) to advisors with a 4-year vesting period

At first, Uniswap airdropped 15% of the total supply of UNI tokens, equal to 150 million tokens, to historical users, including liquidity providers. The table below shows the yearly vesting schedule of UNI tokens allocated to the community.

The treasury does not receive revenue from the protocol itself. Swap fees all go to liquidity providers. The treasury contains only the amount allocated during the token generation event (TGE). The governance treasury retained 43% [430,000,000 UNI] of UNI supply is distributed on an ongoing basis through contributor grants, community initiatives, liquidity mining, and other programs.

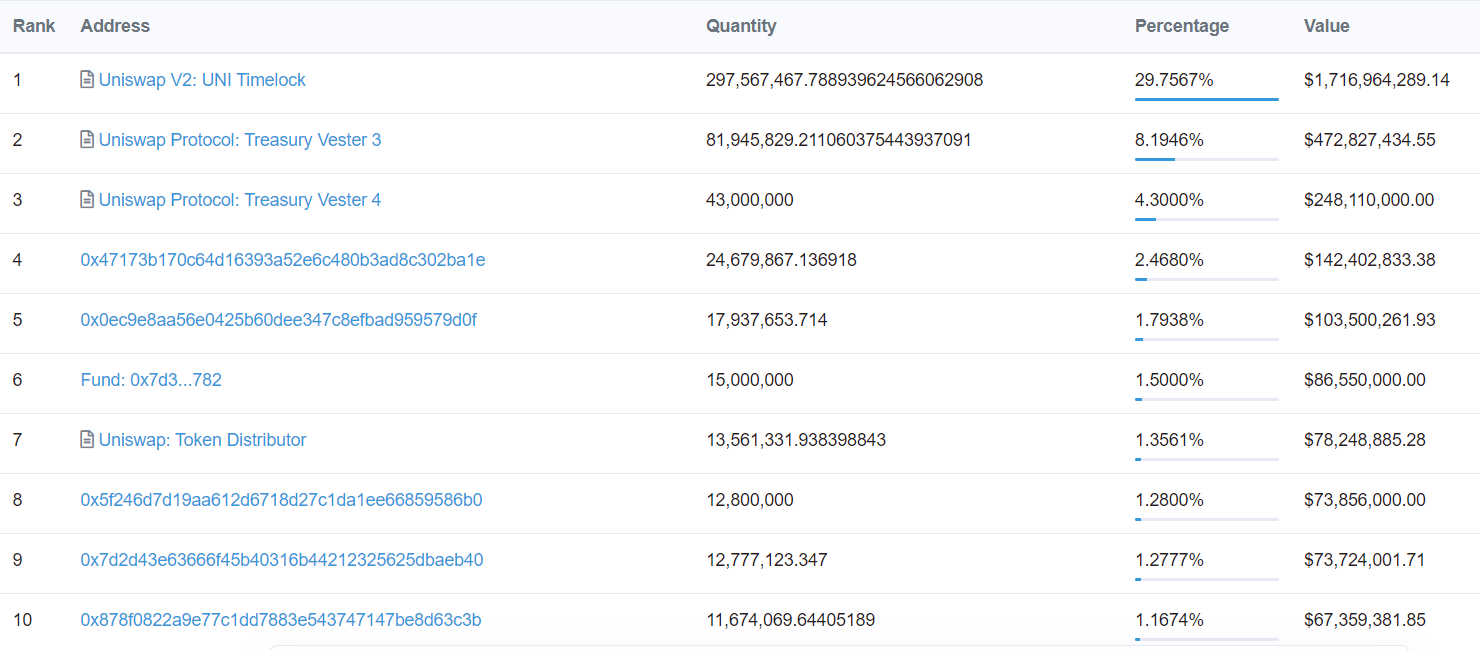

Inspecting the supply's dist among holders, we can measure the wallet concentration to understand the grade of decentralization of the protocol:

The protocol seems relatively decentralized as many top holders are represented by smart contracts treasury.

Below we can compare UNI initial allocation (black dots) compared to other DeFi protocols:

b. Supply schedule & Monetary policy

Those who are generally sitting on profits, having bought the token at a meager price, are undoubtedly the team and the investors who, in this case, account for 39.3% of the total supply. This percentage is significant enough compared to other valuable projects because roughly 40% of the supply is constantly under selling pressure since these stakeholders tend to sell their tokens to realize a profit (and acquired the token at a very low price). Furtherly, notice that team allocation is slightly above that of the investors, these could help the team maintain desired long-term project direction.

But to understand if that is the case, let’s look at the supply schedule.

After four years of reaching a total of 1 billion UNI tokens with a logarithmic emission rate, the supply of UNI is expected to be fully vested by Sept 2024. Afterward, a perpetual inflation rate of 2% per year will ensure continued participation and contribution to Uniswap at the expense of passive $UNI holders. At the time of writing, MarketCap/FDV ratio is around 76%, meaning not so many tokens have to be released yet.

Buying growth with dilution is a good deal whenever the value of the equity grows faster than the issuance rate. And as the value of the equity grows, it costs less and less dilution to acquire more capital.

Source: Placeholder

In turn, the release schedule is well-designed, meaning no specific dates are flooded by new shock emissions, the presence of a long vesting period and the issuance slope decreases over time. The 2% perpetual inflation rate would eventually dilute the token’s value if no incentive mechanisms, e.g. token burns, won’t be adopted.

5. Demand drivers & incentives

Is the token supposed to be held or to be spent?

To answer this question, we should analyze how users interact with the platform, why they use the token, and the incentives fielded by the team.

The Uniswap model is pretty simple: users swap tokens, and LPs supply liquidity to the protocol:

The users are only incentivized to use the platform (and pay fees) if it provides the lowest slippage and a good pool's diversification with enough liquidity.

The LPs lock their funds and earn passive income from swap fees (mainly 0.3% generated off each trade) and can participate in governance processes by locking $UNI to the protocol. It’s pivotal to differentiate locking (just locking the tokens) from staking (locking the tokens and earning revenues by securing the network).

Thus, from the users’ perspective, there is no incentive to keep/hold $UNI (except for speculative purposes) since no advantage exists for swapping purposes (main use case).

From the LPs perspective, since holding $UNI does not allocate a portion of the fee revenue accrued by the liquidity mining to the token holder or even to the treasury, $UNI’s only value capture is governance rights. Indeed, they can vote for a set of protocol delegates which can help to deploy the future direction of the project. Moreover, they vote to add or remove specific token pools for which they can collect fees and modify the fees applied for each pool.

With V3’s improvement in capital efficiency, liquidity providers earn more fees to provide liquidity to the platform. V3’s new algorithm improves trade execution by speed and gas fees. Indeed, LPs can choose the price range they want to provide liquidity to and accrue fees only within this range. This is an excellent incentive to attract more and more liquidity providers to the platform.

Along with the V3 update, a user can now supply liquidity and receive an NFT (ERC-721 tokens) representing his position in the pool (see details here). The minted NFT shows key liquidity position data and differs in the graphics based on the pairs supplied (there is also a small random chance of minted NFT being rare). It can be redeemed at any time in the platform itself or in NFT marketplaces (e.g. OpenSea).

Uniswap’s value comes from its long-standing background, first-mover advantage, and continuous platform development.

The token is supposed to be held (not a spending token) since it guarantees LPs the governance right of which they can take advantage based on their interests.

6. Final thoughts

Uniswap has a unique value proposition and takes advantage of being the first protocol with such unique features, and the team is constantly working to develop the platform. Moreover, the token's design incentivizes holding to gain governance rights over the protocol, its supply it's well-distributed, and the MarketCap/TVL ratio is 1.12, meaning that 88% of the tokens are locked in the contract, keeping the circulating supply low. Furthermore, incentives are fully paid by revenues generated by fees (long-term sustainable) and partially by emitting new $UNI tokens (long-term unsustainable).

Do the incentives create common wealth, and are they value-aligned?

Not enough to me.

The only value-aligned incentive is to lock tokens to grant governance rights. As a result, LPs pursue their interests which, by design, overlap the ones of the protocols. But future improvements can reinforce the value captured by the token (shown in the last paragraph).

a. Risks

To fully evaluate the project, we should highlight some of the associated risks:

Many other players run the same business. Such as are for instance SushiSwap, Curve, and PancakeSwap.

If Uniswap fails to catch LPs for some reason (for example, if another similar platform offers more revenues, like precedent Sushiswap’s vampire attack), there would be fewer LPs to provide liquidity and decreasing in the usefulness for users to keep utilizing the platform.

The treasury is controlled by token holders, including the team and investors. These two categories hold the most significant slice of the pie, potentially allowing them more power than the community.

The only source of treasury’s income was set at TGE with no other than $UNI. If the token falls in price, with no further inflows nor portfolio diversification strategy, it would sharply lose its value causing additional selling pressure as LPs would leave the DAO.

The risk of being hacked. A dedicated incentive program can push white hackers to get back the stolen funds eventually.

[Systemic risk] If some events occur, like big crypto players’ insolvency, this could lead to a massive general token withdrawal which would drain liquidity pools.

b. Ideas for improvement

Even though Uniswap is one of the most relevant and valuable DEX in the crypto space, we can imagine some improvements to capture even more value.

Staking rewards/Revenue sharing: some competitors' DEXs let users lock/stake their tokens to generate passive income in the protocol's tokens*. Such practice must be well balanced considering the net token surplus (supply-demand balance) since it can cause unsustainable inflation.

*Note: if staking the token is just earning you more of that same token, and that token is depreciating (e.g. lack of utility), then you’re not earning anything. You’re just saving yourself from being diluted. One technique to avoid so would be starting from actual earnings (e.g. fees paid by users) to distribute rewards in other tokens.

Governance incentives: good decision-makers inside the DAO should be rewarded, while the bad ones should be slashed. The key is to find objective and measurable KPIs to avoid disputes. SourceCred, for example, is a tool that allows DAOs to measure and automatically reward value creation inside the organization.

Burning mechanism: a percentage of the fees paid by users could be burned using a buy-back and burn mechanism. Given the 2% perpetual inflation rate, this measure allows for slowing down the token emission and the growth (always prefer a steady and slow growth instead of skyrocketing). I found beneficial this article on how to manage treasury funds using a buyback-and-make mechanism instead of buyback-and-burn.

Token flow

Inflow: there is no reason to buy the token from the user’s perspective. Distributing $UNI to token holders (by locking them) each trade, like Sushiswap, can incentivize new buyers.

Outflow: apart from locking tokens to gain voting power, there is no other incentive for holding the token. Additionally, holding a governance utility token is not the best ROI strategy that guarantees users a solid cash flow. Generally, adding additional use cases to the token would increase the circulation of $UNI inside the ecosystem and less selling pressure. Why not reduce LP selling pressure (system token outflow) by switching to Options Liquidity Mining process? Since an LP receives $UNI passively by providing liquidity, he will probably dump them on market to make profits. To manage this situation an example would be setting a buy option (right to purchase) for these tokens to, let’s say, one month (expiry) at price = spot - 50% (strike price). As a result, if for example, the $UNI price after one month loses 50% of its value, LP has no more reason to exercise the option and dump tokens on the market because you have artificially created an additional price floor for the received tokens.

Treasury inflows: the only treasury’s source of income was the allocation at TGE, which is solely composed of $UNI. It could be worth:

To allocate a small % of the generated fees to the treasury. This way, you may discourage LPs (they earn less), so ensure they are equally rewarded (e.g. reinvest such treasury money into holders-oriented initiatives).

To diversify treasury’s portfolio, gaining discretionally exposure to BTC, ETH, and diverse stablecoins.

Thank you for having read my article. If you like it, please follow me on my social pages and tell me how I can improve my content, I’ll be glad to keep your ideas in consideration while writing the next.

ETH wallet for donations: 0x74151366103F899d6FD4200806eC9E9Ee588b5bD

USEFUL LINKS

Sources: I have linked the sources within the text to deepen key concepts useful for full comprehension

Uniswap official blog: https://uniswap.org/blog/uni

CoinMarketCap profile: https://coinmarketcap.com/currencies/uniswap/

CoinGecko Tokenomics data: https://www.coingecko.com/en/coins/uniswap/tokenomics

Messari report: https://messari.io/asset/uniswap

$UNI Token: https://etherscan.io/token/0x1f9840a85d5af5bf1d1762f925bdaddc4201f984

Moonfire tokenomics data: https://tokenomics.moonfire.com/

Nanoly (ex. Coindix) - DeFi aggregator (APY): https://nanoly.com/ethereum

DeFiLlama - DeFi aggregator (TVL): https://defillama.com/

CryptoFees (average spent fees): https://cryptofees.info/

Further reads:

Worth mentioning these two websites (actually in beta version) which let you track several project’s vesting schedules and distribution:

CoinOwl: https://coinowl.io/ongoing-ido

VestLab: https://vestlab.io/