Tokenomics analysis: MakerDAO (MKR-DAI)

Tokenomics analysis: MakerDAO (MKR-DAI)

A DeFi platform - Decentralized lending and algorithmic stablecoin protocol

Index

1. Introduction

This article intends to present MakerDAO key features and tokenomics by providing quantitative and qualitative insights to better evaluate the project for academic/research purposes. At the bottom of the article, you can find helpful links to deepen project knowledge.

Previously I have written a similar article about Uniswap tokenomics which I suggest to read.

This is not financial advice; always DYOR.

Maker (MKR) is a permissionless, multi-asset, overcollateralized smart contract lending platform based on the Ethereum blockchain (layer 1). It allows users to take out decentralized loans by locking-in collateral in exchange for $DAI (algorithmic stablecoin issued by the protocol pegged to 1USD). On the other hand, $MKR represents a fungible governance token (a type of utility token) useful for assigning users governance rights and acting as a form of protection against liquidation events. The Maker protocol is one of the earliest projects (Dapp) in the Decentralized Finance (DeFi) ecosystem.

It was founded by Rune Christensen in 2015 as an open-source project to offer economic freedom and opportunities to anyone, especially to the unbanked people. Indeed, users don’t need to perform the know-your-customer (KYC) process. The only thing required is a collateral asset (generally crypto-assets) to secure the loan.

A user can borrow a certain amount of stablecoin ($DAI) by locking some collateral to a smart contract and paying interest (stability fee) on such a loan. Since the mechanism relies on decentralized entities as a form of guarantee, the collateral value at the time of the loan must be higher (over-collateralization) than the borrowed stablecoin value. If a collateralized asset value declines, the user is requested to add more collateral or close the position. Otherwise, he receives a liquidation penalty and has to pay accrued stability fees + liquidation amount from its collateral value. Currently, Maker supports different asset types as collateral, and it started a process to include Real World Assets (RWA).

Furthermore, users can deposit stablecoin ($DAI) into the protocol and receive interest based on the DAI Savings Rate (DSR). Moreover, Maker offers users to swap stablecoins pairs (e.g. DAI-USDC, DAI-GUSD) through its Peg Stability Module (PSM).

At the time of writing, MakerDAO counts around $6.8 billion in Total Value Locked (TVL), first in the DeFiLlama TVL ranking list with a 15.7% market dominance compared to the entire DeFi ecosystem.

2. Key scores

Before going forward with the analysis, here you can find a summary of key metrics to evaluate the project’s health quickly. Remember that these scores are subject to my evaluation except for grey and red ones.

3. Protocol

a. Evolution

The project was conceived in 2015 and fully launched in December 2017. MakerDAO was intended to create a decentralized organization leveraging a stablecoin ($DAI) with a stable value soft-pegged to the US dollar.

In 2017, it launched the Maker governance token ($MKR) and its first decentralized stablecoin, Single Collateral Dai (SAI), issued with Ether only as collateral.

The MakerDAO Foundation released the Multi-Collateral Dai (DAI) two years later. The platform then gained massive adoption and soon became the largest decentralized lending platform, with around $2.6B in total value locked (TVL) as of the end of 2020.

As of October 2020, $DAI became one of the most popular stablecoins in the crypto market, and nowadays shows off 15.7% market dominance compared to the entire DeFi ecosystem owning the highest TVL.

b. Protocol description

As we stated, Maker is a decentralized lending platform that works by issuing new $DAI backed by an over-collateralized asset. $MKR instead represents the governance token, used to manage the issuance of $DAI.

Let’s first introduce some key concepts before making an example.

Vaults: MakerDAO enables borrowing through the creation of Vaults. When a user opens a Vault means he’s depositing collateral to borrow $DAI stablecoin.

Stability Fee: A variable-rate fee represents the interest a user owes to borrow $DAI. The Stability Fee cannot be negative, and it’s compounded per second.

DSR: The $DAI Savings Rate allows any $DAI holder to earn savings automatically by locking their $DAI into the DSR contract in the MakerDAO protocol.

Liquidation Penalty: it is a fee the user pays when the value of the collateral hits the Vault’s Liquidation Price. This price is set so as to safely close the debt position to repay the borrow + interest fees in full, and it depends on the collateral asset’s volatility (the more volatile the asset is, the tighten liquidation price will be).

Keepers: they participate in auctions resulting from liquidation events, acquiring collateral at attractive prices. The system incentivizes early bidders to repay the user loan.

Now, let’s try to understand the mechanism with an example:

A user opens a new position (Vault) with 10 ETH as collateral. Let’s assume its current market value is $10.000 (meanings 1.000 $ETH price).

Such a user will then receive 5.000 $DAI (the Principal) by assuming the current collateralization ratio is 200%. The user can reinvest the borrowed $DAI into other DeFi platforms to earn more revenues (useful until earning APY > stability fee APY).

The user contracts a debt he must repay based on the applied annual interest rate (stability fee). The liquidation ratio is 150% (meanings the user will be liquidated if the collateral value falls to 7.500$).

Here are the following scenarios:

Surplus Auction: loan < collateral (Best case for $MKR holders)

Here is the case in which a user can repay his debt. MakerDAO gets stability fee profits

Whenever the net surplus from stability fees reaches a certain threshold, the surplus $DAI is auctioned off on an external DEX. Keepers offer a certain amount of $MKR for the $DAI accrued, then Maker burns them, thereby reducing the amount of $MKR in circulation. No human intervention is needed since smart contracts execute the entire process automatically.

Collateral Auction: loan <= collateral (Neutral case for $MKR holders)

Here is the case where a user can repay his debt but falls below the liquidation price threshold. MakerDAO gets a stability fee + liquidation penalty profits.

The Vault is liquidated when the collateral value has fallen below the liquidation price. Then, a collateral auction is triggered. In this case, the collateral value is below the liquidation price but higher than the total value of debt (principal + accrued stability fees). In turn, keepers bid any amount of $DAI to acquire part of the collateral value and, at the end of the auction, the protocol keeps the principal plus stability fees plus liquidation penalty and returns the leftover collateral (if any) to the borrower.

Debt Auction: loan > collateral (Worst case for $MKR holders)

Here is the case where a user cannot repay his debt because the collateral value rapidly decreases below the principal value. MakerDAO gets the residual collateral and mint new $MKR to repay the debt.

When the collateral price drops sharply below the principal value, the system initiates a debt auction to cover the losses, whereby the winning bidder pays $DAI to cover the outstanding debt. In return, he gets a certain amount of newly minted $MKR, increasing the amount of $MKR in circulation.

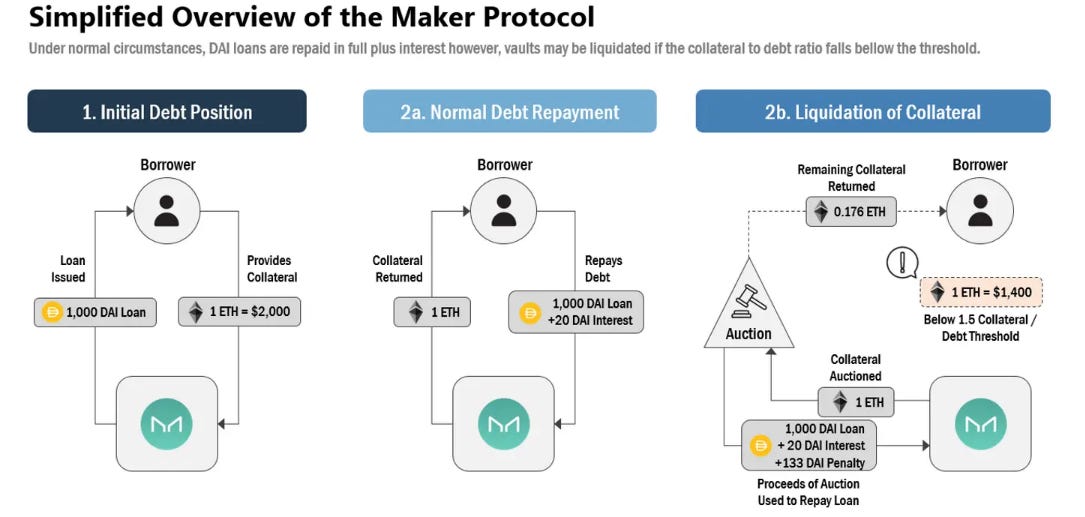

Below is a simplified overview of the processes explained above:

Other use cases are applicably interacting with the protocol; they are:

Deposit and locking $DAI to earn interest based on Dai Savings Rate (DSR)

Swap $DAI with other stablecoins through the Peg Stability Module (PSM)

When the market price of $DAI deviates from the Target Price of 1$, Maker’s holders, through a governance process, can mitigate the price instability by voting to adjust the DSR accordingly:

If the market price of $DAI is above 1$, they will gradually decrease the DSR to reduce the demand for the stablecoin and thus reduce the price of $DAI until it is re-pegged to the 1$ target price.

If the market price of $DAI is below 1$, they will instead opt to gradually increase the DSR to increase the demand for the stablecoin and thus increase the price of $DAI until it is re-pegged to the 1$ target price.

Finally, a user can swap $DAI for other stablecoins (e.g., GUSD, USDC) without taking any debt or needing to manage a Maker vault. From a user’s perspective, it works just like an automated market maker (AMM) with a liquidity pool behind it.

Instead, the Peg Stability Module (PSM) is a particular type of Vault that allows users to swap collateral for $DAI rather than borrowing $DAI against collateral, thus controlling demand for $DAI through arbitrage and hence restoring its peg.

The PSM is intended to absorb short-term $DAI peg deviations. Instead, the system should adjust the supply and demand of $DAI for long-term health using the DSR mechanism.

Furthermore, an emergency tool called Emergency Shutdown Module (EMS) exists. It allows MKR holders to shut down the protocol by instantly burning 100K $MKR. The tool is helpful either under a malicious governance attack or in the event of a critical bug.

c. Value proposition

While Maker does not pay dividends to their holders, MKR’s unique proposition is that it allows its holders to participate directly in governing DAI protocol.

Every holder of Maker tokens has some voting power, depending on the size of their MKR stake, on several proposals to the Maker Protocol. Some of the aspects of the protocol the holders can vote on are:

Adding new collateral asset types. Users can then submit new cryptocurrencies (or RWA) to mint more $DAI.

Modifying the collateralization ratio of existing collateral assets.

Changing the DSR to manage the profitability of the $DAI saving contract.

Adjusting the stability fee.

Choosing the oracles.

This ability to participate in managing one of the most significant stablecoins protocols on the market drives the demand for $MKR. Even if the governance choices are not direct actions on $MKR holder cash flow (Uniswap holders, for example, can choose transaction fee parameters on the pools), they can impact how and through which parameters $MKR is minted or burned. This affects the circulating supply, making the token scarcer or not, impacting the $MKR price.

The protocol’s revenues are derived from the following primary sources:

Lending income: interest revenues from loans (Stability Fees)

Liquidation income: liquidation revenues from liquidated vaults

Trading fees: stablecoin trading fees from the PSM

Below there is a demand-risk schema to understand the unique selling proposition (USP) and what factors could affect it:

d. Benchmark

Since MakerDAO offers lending/borrowing services other than stablecoins’, some of its competitors are AAVE, Compound, and Venus.

AAVE ($AAVE) is another decentralized finance protocol that allows users to lend/borrow crypto assets and support different chains (including Ethereum, Polygon, Avalanche, and Fantom). Lenders earn interest by depositing digital assets into liquidity pools, while borrowers can use their crypto as collateral to take out loans. The holders are incentivized to use the platform with discounted fees. It also serves as a governance token giving owners the right to be decision-makers in the protocol’s development.

Compound ($CMP) is another DeFi lending protocol (it works only in the Ethereum network) that allows users to earn interest by depositing crypto assets into several pools supported by the platform. When a user deposits tokens to a pool, he receives cTokens in return. This type of token represents the individual’s stake in the pool and can be used to redeem the underlying asset initially deposited. The interest is compounded into the token value itself since, once received, the exchange rate of it increases over time. In Compound, there are similar rules to those explained before to manage the maximum loan-to-value (LTV) ratio and liquidation thresholds. Compound incentives its users to borrow by giving them $CMP.

The main difference between Maker and its competitors (AAVE and Compound) is that they exploit a two-sided mechanism - lenders for supplying liquidity and borrowers for using it - instead, Maker only allows a user to borrow against his own collateral or swap stablecoin pairs.

Finally, Venus ($XVS) is an algorithmic money market and synthetic stablecoin protocol launched exclusively on the Binance Smart Chain (BSC). The protocol offers an elegant crypto-asset lending/borrowing solution to the DeFi ecosystem, enabling users to perform a variety of use cases at high speed and low transaction fees leveraging the BSC. In addition, Venus allows users to mint $VAI stablecoins (BEP-20 standard) by posting at least 200% collateral to the smart contract. Additionally, $XVS holders have governance rights over the protocol.

Below is a comparison table among main Maker competitors highlighting some standard DeFi metrics.

4. Supply metrics

As per Maker tokenomics, let’s first discuss the key metrics affecting the token’s supply and then try to understand if Maker’s incentives are value-aligned with the product and help create a common wealth within the ecosystem.

Below are the main $MKR supply data and volumes generated so far:

Likewise for $DAI supply metrics:

a. Distribution

Maker launched with 1,000,000 $MKR tokens (uncapped max supply) and distributed them to early adopters and investors through three subsequent private sales starting in November 2017 until Dec 2019 (the last private sale session). The initial token distribution (TGE) of Maker is as follows (pre-mined token launch):

69.5% (690.500 $MKR) to Founders & Project (early adopters, ecosystem, treasury)

15% (150.000 $MKR) to the Team

4% (40.000 $MKR) to Seed Round 1 (investors)

6% (60.000 $MKR) to Seed Round 2 (investors)

5.5% (50.500 $MKR) to Seed Round 3 (investors)

Inspecting the supply’s dist among holders, we can measure the wallet concentration to understand the grade of decentralization of the protocol:

The protocol looks decentralized as many top holders are represented by smart contracts treasury.

b. Supply schedule & Monetary policy

The below diagram illustrates the Net burned $MKR (total burned - total minted) on a quarterly basis:

Instead, the below chart shows, quarterly, the total $DAI supply issued so far:

The total supply of $MKR (no hard-coded limit) can increase if a deficit is triggered by “bad loans” and needs to dilute the token as a recapitalization source. If the system is well governed, the total amount of $MKR will decrease as it is destroyed in exchange for excess $DAI from the system’s surplus. This ensures that $DAI is always fully collateralized and its peg to the USD is maintained. Below you can find Maker’s supply schedule:

Thus, the supply of $MKR is a dynamic value that changes depending on market conditions, lenders’ trust, and the overall health of the DAI ecosystem.

Maker has a unique and variable release schedule depending on the market conditions and on the $DAI peg mechanism. No annual inflation rate is predictable. No max cap is set (ideally, it should remain at around $1M token), and his MarketCap/FDV shows a solid score of 97%.

5. Demand drivers & incentives

Is the token supposed to be held or to be spent?

To answer this question, we should analyze how users interact with the platform, why they use the token, and the incentives fielded by the team.

Maker offers users the chance to borrow a certain amount of stablecoin $DAI at a stability fee rate by over-collateralizing their crypto assets. There are three different scenarios, as explained in the Protocol section, which would affect the issuance of $MKR. We can reduce them to two macro cases:

Best case

Better $DAI lending decisions → higher stability fees generated → more $MKR bought and burned → reduction of $MKR in circulation → appreciation in $MKR price.

Worst case

Poor $DAI lending decisions → losses incurred by the system → additional $MKR minted to cover the losses → increase in $MKR in circulation → depreciation of $MKR prices.

The demand for $DAI depends on the market conditions, and the supply (demand in turn) can be adjusted accordingly (through DSR). Arbitrageurs are encouraged to bring back the peg of $DAI each time it deviates from the one-dollar value. As a result, the demand for $DAI influences the demand for $MKR in a very sophisticated balance mechanism.

Since the protocol’s revenues mainly come from:

Lending: interest revenues from loans

Liquidation: liquidation revenues from liquidated vaults

Trading fees: stablecoin trading fees

Such revenues increase the value of the token holders; the demand is shaped by the protocol (e.g., by the governance) around these parameters:

Stability fee

Collateral liquidation price

Asset collateralization ratio

DSR

PSM

Another protocol’s use case impacts the Keepers who participate in auctions due to liquidation events, and thereby they are encouraged to acquire collateral at an attractive price. Of course, it is worth mentioning again that the main Maker’s incentive relies upon the governance utility of the token.

The last recent demand driver Maker has put in place is the extension of collateralized asset types. Since Terra, a late entrant onto the scene was almost double the $DAI market cap in March 2022, a few weeks before it imploded, the DAI community was forced to take some measures to remain relevant in the changing stablecoin environment. Of the community’s multiple initiatives to increase $DAI adoption, the most notable one was onboarding more Real World Assets (RWA) as collateral. By adding RWA as collateral, Maker would expand the types of collateral against which $DAI can be borrowed on the platform, which, in turn, it translates into new potential loans originating from the platform.

New loans → collection of more fees → reduced availability of $MKR → higher market value of $MKR

The token $DAI is supposed to be spent since it represents a medium of exchange for the entire crypto ecosystem.

The token $MKR is supposed to be held since it guarantees owners governance rights of which they can take advantage based on their interests and the protocol itself.

6. Final thoughts

Maker enjoys the first-mover advantage of being one of the former lending systems and well-structured DAO protocols in the entire DeFi ecosystem. It has demonstrated resilience against competitors’ initiatives in a fast-changing environment, and the demand is robust due to several incentives the users can leverage. While the $DAI demand relies on arbitrageurs’ hands, the $MKR value depends on the quality of the borrows the protocol is capable of. Meanwhile, MakerDAO has the highest TVL and dominates the market, owning 15.7% of the total DeFi ecosystem value. Its Market capitalization is very close to the corresponding Fully diluted market value.

Do the incentives create common wealth, and are they value-aligned?

Surely.

The protocol growth is well-addressed by initiatives like RWA extension, which would increase the demand for $DAI. Increased $DAI demand leads to higher borrowing requests and, thus, more revenues for the protocol in the form of:

More $MKR burns from stability fees

More $MKR burns from liquidations

More trading fees from stablecoins swaps

The protocol offers incentives for the keepers to optimize liquidation procedures and spur arbitrageurs to maintain the $DAI peg. Governance rights are desirable by token holders since they would manage billions in their treasury. The tokens binary mechanism is well-designed, the balance in the system is kept steady and one's demand ($MKR) is reinforced by the other's ($DAI) by establishing a virtuous circle.

To note that by continuously burning $MKR, this would appreciate in price since circulation supply tends to decrease, but it doesn’t change the overall value of the system itself. Indeed, it only redistributes current value among a smaller group of people. A lot of buybacks are often associated with low growth.

Slow and steady wins the race

a. Risks

To fully evaluate the project, we should highlight some of the associated risks:

Many other players run the same business. Such as are for instance AAVE and Compound. Their actions could lead to a different Maker’s monetary policy, which could erode the profitability of the protocol.

If Maker fails to maintain the $DAI peg, it could lead to a massive user withdrawal, resulting in a $MKR value loss.

If the rate of burning ever outpaces the system growth rate, there is a risk of temporarily decapitalizing the system by consolidating ownership too tightly at the expense of liquidity and long-term value.

Risk to contract bad loans for which borrowers would not be able to repay their debt, forcing, in the worst-case scenario, an increased $MKR issuance rate.

[Decentralization risk] The governance is fully in the hands of token holders. If they fail to adequately set stability fees, DSR, and liquidation ratios, then it would affect revenues in the form of diluted $MKR value.

The risk of being hacked. A dedicated incentive program can eventually push white hackers to get back the stolen funds. It is worth mentioning Maker relies on an emergency tool called Emergency Shutdown Module (EMS) which could be used either under a malicious governance attack or in the event of a critical bug.

Being too exposed to certain collateral assets would increase the risk of dependency (poor assets diversification).

[Systemic risk] If some events occur, like big crypto players’ insolvency, this could lead to a massive general token withdrawal which would drain the TVL in the platform.

b. Ideas for improvement

We can imagine some improvements to capture even more value:

Collateral diversification portfolio: one of the protocol goals should be lowering the risk of being too much dependent on certain assets. Allowing users to deposit increasingly collateral classes (valuable crypto assets, RWA, …) could help mitigate the depreciation risk of a specific asset influencing the protocol and from a black swan event that is localized to that asset. Ideally, a single asset should not exceed X% (or X $DAI units) of all $DAI collateralization vaults (debt ceiling). No “bad” illiquid assets should be accepted as collateral to decrease the risk of liquidation.

Decentralization: On Sept 22, a proposal received a green light: to move $1.6 billion worth of $USDC from Maker’s reserve into Coinbase Prime, which will allow the protocol to lock in and earn a 1.5% yield on its assets. This runs contrary to the intention to decentralize stablecoin holdings.

To mitigate the centralization risks exposure, the protocol could counterbalance such an amount by allocating other funds to DeFi low-risk solutions with similar yields (e.g. other algorithmic stablecoins lendings, stablecoins LPs, ETH staking on Lido, …).

Democratic voting process: implementing a quadratic voting mechanism (QV) can further democratize the governance process and avoid a concentration of MKR tokens. Keeping simple: your voting power is equal to the square root of your staked tokens. If you own 64 $MKR your voting power will be 8 while owning 16 $MKR guarantees you 4 votes.

It protects minorities, helps balance power among holders, and could lead to a better capture of community sentiment when compared to rank-choice voting.

Hodling stimulus: further token value generation could derive from the $MKR holding age. Longer staked coins could gain more “weight” for voting processes accrued, for example, in the form of mToken*. This is an incentive to lock up the tokens as much as possible further reducing the circulating supply. This measure could be used, in a balanced way, together with the previous one, since:

QV → tends to democratize the governance process (DAO’s goal-aligned) but at the same time discourages further token holdings (accumulation disincentive)

Hodl stimulus → on one hand, it stimulates lock-in mechanisms (holding incentive) by mostly rewarding old-aged token holders, on the other hand, it discourages late entrants.

Pursue DAO’s goal —> Enabling Hodl incentives —> By not concentrating the power

*mToken could work similarly to cToken (in the Compound protocol) which accrues interest over time but, in this case, it accrues voting power instead. Keep in mind $MKR is a governance token (not a spending one), so this incentive is in line with the token utility.

Undercollateralized loans: stating that Maker is approaching to accept RWA, such loans could also be undercollateralized to better incentivize institutional money inflows and to unlock capital efficiency in DeFi. To guarantee the quality of the loan the borrower has to provide cryptographically signed messages from wallet addresses to prove it has possession of a requisite amount of funds (like proof of reserve) and monitor these addresses in order to ascertain whether or not it is adhering to the covenants laid out in the agreement. Additionally, to enforce an immutable cash flow schedule, automatic tiered payments and liquidations (smart contract based) should be used. To further reduce the insolvency risk, a credit assessment process must be conducted, and only then a legally-binding loan agreement must be signed. The lender should diversify the borrowing entities in such a way the default or bankruptcy of one borrower only jeopardizes a portion of the pool’s funds. Maple and TrueFi are two examples of unsecured lending platforms.

Goes without saying that these initiatives deviate a lot from the idea of decentralization Maker has always pursued. Either way, the experimentation between TradFi and DeFi can lead to great progress in the future and bring more and more adoption.

Thank you for having read my article. If you like it, please follow me on my social pages and tell me how I can improve my content. I’ll be glad to consider your ideas while writing the next one.

ETH wallet for donations: 0x74151366103F899d6FD4200806eC9E9Ee588b5bD

Sources: I have linked the references within the text to deepen key concepts useful for complete comprehension

MakerDAO official blog: https://blog.makerdao.com/

CoinMarketCap profile: https://coinmarketcap.com/currencies/maker/

CoinGecko Tokenomics data: https://www.coingecko.com/en/coins/maker/tokenomics

Messari report: https://messari.io/asset/maker

$MKR Token: https://etherscan.io/token/0x9f8f72aa9304c8b593d555f12ef6589cc3a579a2

$DAI Token: https://etherscan.io/token/0x6B175474E89094C44Da98b954EedeAC495271d0F

Maker burn: https://makerburn.com/#/charts/mkr-and-burn

$DAI stats: https://daistats.com/#/overview

MakerDAO technical docs: https://docs.makerdao.com/

Nanoly (ex. Coindix) - DeFi aggregator (APY): https://nanoly.com/ethereum

DeFiLlama - DeFi aggregator (TVL): https://defillama.com/

CryptoFees: https://cryptofees.info/

Staking rewards: https://www.stakingrewards.com/earn/makerdao/

Chainlist (add new chain/network to a wallet): https://chainlist.org

Buyback-and-make mechanism: https://www.placeholder.vc/blog/2020/9/17/stop-burning-tokens-buyback-and-make-instead

Tokenomics of DAOs: https://tokenomicsdao.xyz/blog/tokenomics-101/tokenomics-101-daos/

Further tokenomics resources: https://fstrauf.github.io/tokenomicsDAO/basic_resources/