Tokenomics analysis: GMX

A DeFi derivative platform - Decentralized spot & perpetual swap exchange (DEX)

Index

1. Introduction

This article intends to present GMX’s key features and tokenomics by providing quantitative and qualitative insights to better evaluate the project for academic/research purposes. At the bottom of the article, you can find helpful links to deepen project knowledge. Look at my previous Uniswap & MakerDAO tokenomics analysis.

This is not financial advice; always DYOR.

GMX is a decentralized (DeFi protocol) spot and perpetual swap exchange that supports low swap fees and zero price impact trades. Perpetual contract traders could use up to 30X leverage on the GMX exchange. The trading experience resembles the functionalities of centralized exchanges, but it’s done directly through a non-custodial wallet, with lower fees and faster trade settlement times. In addition, GMX uses Chainlink oracles for dynamic pricing to aggregate prices from other relevant exchanges without having a single point of failure.

The protocol has a native token called $GMX, which functions as a governance, utility, and value-accrual token. Trading is supported by a unique multi-asset pool (called “GLP”) that earns liquidity providers’ fees generated through market making, swap fees, leverage trading (spreads, funding fees & liquidations), and asset rebalancing. Token holders receive such fees in different proportions.

$GLP, instead, is the value-accrual liquidity provider’s token issued when a user locks collateral into the platform.

GMX currently supports Arbitrum and Avalanche networks but plans to expand the list of supported ecosystems.

At the time of writing, GMX counts around $808 million (staked tokens included) in Total Value Locked (TVL) and is 16th in the DeFiLlama TVL ranking list.

2. Key scores

Before going forward with the analysis, here you can find a summary of key metrics to evaluate the project’s health quickly. Remember that these scores are subject to my evaluation except for grey and red ones.

3. Protocol

a. Evolution

GMX first launched on the Arbitrum One blockchain in September 2021. Arbitrum is an Ethereum layer-2 Rollup, a solution designed to boost the speed and scalability of Ethereum smart contracts.

During the first months since its inception, the team improved pricing contracts mechanisms, and users are able to trade with much smaller spreads. Furthermore, as suggested by the community, they added fee discounts based on a referral program. The platform has increasingly accepted different tokens as collateral, such as $LINK, $UNI, and $USDT.

Later, in January 2022, the protocol expanded its capabilities and launched on the Avalanche network, a high-speed EVM-compatible blockchain that drastically reduces trading fees.

There is not much information about the team behind GMX. The project could be led by a certain Gambit Financial, a spot and perpetual exchange on Binance Smart Chain. GMX is a rebrand from the now deprecated Gambit exchange.

b. Protocol description

The platform allow users to:

Simple swap tokens

Trading operations

Earn with yield compounding

I won’t go into the swap process’ details as it is not a core feature of the protocol. However, you can learn about AMM (Automated Market Making) in my article on Uniswap.

TRADING

For trading purposes, a user can buy or sell the supported assets through the following instruments:

Market takes (market orders)

Market makes (limit & stop orders also with leverage*), specifically:

In practice, GMX allows users to operate just like a CEX but in a decentralized environment with minimum fees and no impact on prices.

*Be aware of the liquidation risk when using this financial product.

Below you can find the number of active daily traders on GMX:

EARNINGS

From an earning perspective, GMX boasts a unique incentive system that makes its main token ($GMX) very attractive for long-term holding, thus optimizing the project’s tokenomics. We can ease the primary platform’s building blocks into four:

GMX token

esGMX token

GLP token

Multiplier Points (MP)

GMX TOKEN

$GMX is a utility and governance token. Every token holder has voting rights — see the Demand Drivers & Incentives section below for further details. Users can choose to stake their tokens and get three additional rewards:

Participate in 30% of all generated protocol fees. These fees are collected from market making, swap fees, and leverage trading and are paid in ETH (Arbitrum network) or AVAX (Avalanche network).

Earn escrowed GMX (esGMX) tokens. These can be staked for rewards or vested to gain other $GMX.

Earn Multiplier Points (MP) that boost the yield. These MP reward long-term holders without contributing to token inflation.

esGMX TOKEN

A user can earn such tokens by staking $GMX or $GLP. If staked, they accrue rewards in terms of the following:

Participate in the 30% of all generated protocol fees (compounded to the fees received for GMX/GLP staking alone).

Earn additional escrowed GMX (esGMX) tokens (compounded to the esGMX received for GMX/GLP staking alone).

Earn Multiplier Points (MP) that boost the yield (compounded to the MPs received for GMX/GLP staking alone).

The esGMX tokens can also be vested. In this case, the GMX/GLP staked are reserved, and esGMX no longer accrues the above staking rewards. Instead, staked GMX/GLP continues to accrue staking rewards. During following 12 months, vested esGMX gets converted back into $GMX.

GLP TOKEN (Liquidity Providers)

At the core functionality of the exchange is a community-owned multi-asset liquidity pool — the GLP pool. Contrary to some liquidity pools, GLP suffers no impermanent loss. The Automated Market Maker (AMM) algorithm uses the pool to serve the decentralized spot exchange (swap) and perpetual contract services. Perpetual contract traders can borrow up to 30X the value of their collateral from the GLP pool.

A user can choose to lock assets in the pool — currently supports ETH, (w)BTC, UNI, LINK, AVAX, and some significant stablecoins such as DAI or USDC — and mint $GLP, which represent the user’s stake in the pool. Newly minted $GLP are automatically staked and provide earnings to the user:

Participate in the 70% of all generated protocol fees. These fees are collected from market making, swap fees, and leverage trading and are paid in ETH (Arbitrum network) or AVAX (Avalanche network).

Earn escrowed GMX (esGMX) tokens.

A user can close the position and withdraw supplied collateral at any moment, which triggers a $GLP burn. That is the case with a non-inflationary tokenomics model since incentives do not directly yield newly minted $GMX.

Note that the GLP pool is a counterparty to the traders. As GLP token holders provide the liquidity used for leverage trading, they profit when traders lose and vice-versa.

Additionally, the protocol uses a rebalancing mechanism to control the applied fees to mint/burn/swap $GLP based on whether the action improves the balance of assets or reduces it. Token weights, available in the Dashboard, are promptly adjusted to help hedging strategies of GLP holders based on the open positions of all traders.

Multiplier Points (MP)

If users stake GMX/esGMX, they earn Multiplier Points at 100% APR (i.e., staking 200 $GMX tokens for one year earns you 200 MP). The MPs can also be staked to boost actual ETH/AVAX APRs accrued from GMX/esGMX staking). When the GMX/esGMX tokens are unstaked, the MPs are burnt.

You can find every detail inherent to operational trading on the platform here.

Finally, it also established a Floor Price Fund that helps ensure liquidity in the GLP pool and provides a reliable stream of $ETH rewards for GMX stakers. As the floor price fund increases, it could be used to buy-back and burn $GMX if the Floor Price Fund/Total GMX Supply is less than the market price of GMX. This would set a minimum floor price for $GMX in terms of $ETH and $GLP.

c. Value proposition

GMX provides users with unique features:

Minimal liquidation risks

The GMX aggregate of high-quality price feeds (Chainlink) determines when liquidations occur and keeps positions safe from temporary wicks.

Low costs

GMX allows users to enter and exit positions with minimal spread and zero price impact. This design may help traders get better entry prices than some order book-based exchanges, which might have issues with slippage.

Simple swap

GMX users can open positions through a simple swap interface. This function lets users conveniently swap from any supported asset into the position of their choice.

Capital efficiency

Its dual exchange model supports both spot swaps and leveraged trading of perpetual swaps, improving capital efficiency due to the high asset utilization of the GLP pool, which lets user deposits generate extra yield and not sit idle.

In addition, there are several GMX community-built tools and calculators available for traders which facilitate the user’s experience interacting with the platform:

Telegram positions bot

The gmx.house leaderboard

The gmxstats.com page

Dune analytics dashboards

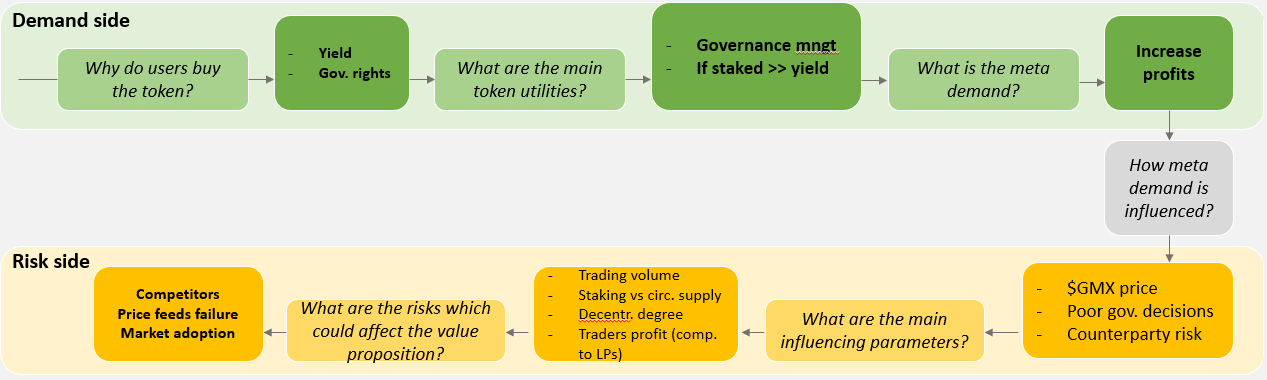

Below there is a demand-risk schema to understand the unique selling proposition (USP) and what factors could affect it:

d. Benchmark

Despite its unique features, GMX has to encounter the competition, among which are:

Launched in 2017, dYdX is a DEX that runs smart contracts only on the Ethereum network to offer perpetual contract trading, margin trading, spot trading, lending, and borrowing services by providing collateral.

It counts around $435 million in Total Value Locked, is 24th in the DeFiLlama TVL ranking list, and benefits by being the first mover. Similarly to GMX, an investor can provide liquidity to dYdX’s trading pool to receive rewards.

There are some differences compared to GMX:

A user can only send USDC as collateral to the platform.

There is only one token, $DYDX

dYdX incentivizes users through a trading rewards program, where they receive $DYDX based on their trading activity.

Gains network is a decentralized perpetual exchange on Polygon. It launched gTrade, a decentralized leveraged trading platform with synthetic assets. Unlike dYdX and GMX protocols, these synthetic assets enable it to offer a wide range of leverages and pairs (up to 150x on cryptos, 1000x on forex, and 100x on stocks).

On Gains Network, the investor can provide liquidity to the vault (only in the form of $DAI) used as a counterpart to the trading activity and receive rewards. Gains Network also uses a referral program to boost its daily average number of users.

The protocol has two tokens:

$GNS (ERC-20 token): $GNS holders receive platform fees when staking through Single Sided Staking, paid in $DAI.

GNS NFTs (ERC721 utility token). NFT holders get reduced spread and boosted rewards on top of the regular ones.

Below is a comparison table among the threes highlighting some standard DeFi metrics.

4. Supply metrics

As per the protocol tokenomics, let’s first discuss the key metrics affecting the token’s supply and then try to understand if GMX incentives are value-aligned with the product and help create a common wealth within the ecosystem.

Below are the primary $GMX supply data and volumes generated so far:

a. Distribution

The Initial token distribution (TGE) of $GMX is as follows:

45.28% (6.000.000 $GMX) allocated to XVIX and Gambit migration 15.09% (2.000.000 $GMX) allocated to the Floor Price Fund (to maintain GLP pool and ETH reserves)

15.09% (2.000.000 $GMX) allocated to reserve (for vesting from esGMX rewards).

15.09% (2.000.000 $GMX) allocated to liquidity (paired with ETH for liquidity on Uniswap)

7.55% (1.000.000 $GMX) allocated to the presale round

1.89% (250.000 $GMX) allocated to marketing & partnership (distributed to contributors linearly over two years)

Following the GMX exchange’s rebranding from Gambit and merging XVIV tokens, over 45% of the GMX token supply belongs to old Gambit and XVIX holders who migrated their tokens to GMX.

Inspecting the supply’s dist among holders, we can measure the wallet concentration to understand the grade of decentralization of the protocol:

With more than 184.000 unique holders, the protocol looks decentralized as smart contracts’ treasury/liquidity represents many top holders. In particular, note that the first contract, which held 75% of the tot supply, is responsible for managing the staking process and handling rewards to the users. By the way, be aware that the team controls many parameters which can be enforced without governance approval (they can also pause trading using an admin key).

b. Supply schedule & monetary policy

The forecasted max supply of $GMX is 13.25M, with around 8.2M circulating.

Anyway, the increase in circulating supply will vary depending on the number of tokens (esGMX) that get vested and the number of tokens used for marketing and partnerships. In any case, minting new tokens beyond the 13.25M threshold could be possible only after a governance acceptance process, and new issuance will have a 28 days timelock. Below you can find proposed token emission for 2022:

At the time of writing, MarketCap/FDV ratio is around 63%, meaning so many tokens have yet to be released and no hard-cap being encoded in the smart contract. Below you can find the cumulative emission so far. From this chart, we can derive the estimated inflation rate of 18% since Nov 2021 (note that this is not a linear emission and the slope can change based on the statements described before).

The new issuance is almost entirely reflected by the actual vesting process, which will turn esGMX into GMX after a year, around 37% are yet to be released. Furthermore, since users have vested their tokens in different epochs, no specific dates are flooded by new shock emissions. Finally, more than 84% of the circulating tokens are currently staked (for yield compounding), so there is a supply shortage, leading to buying pressure.

5. Demand drivers & incentives

Is the token supposed to be held or to be spent?

To answer this question, we should analyze how users interact with the platform, why they use the token, and the incentives fielded by the team.

Token holders: are incentivized by governance rights over the protocol and rewards in terms of esGMX, MPs, and sharing protocol fees (30%) if the token is staked.

Liquidity providers: are encouraged to supply collateral (i.e., mint $GLP, which is automatically staked) to increase GLP pool size by receiving esGMX and participating in a consistent percentage (70%) of the protocol fees.

Traders: GMX allows future perpetual trading whose market size is far more vast than the spot market. Furthermore, the protocol’s referral program drives adoption by incentivizing new users’ onboarding, generating discounts and rebates for the referral code owner.

The protocol’s revenues come from the following primary sources:

Swap fees: fees paid for swapping tokens into the platform (range from 0.2% - 0.8% depending on asset composition of GLP pool).

Trading fees:

Trading fees: when a user sends a transaction to request open/close/deposit or withdraw collateral (0.1% of the position size for each trading operation).

Execution fees: paid to the keepers (in ETH/AVAX) to execute the trade.

Liquidation fees: if collateral for leveraged position drops below the liquidation price, keepers close the position and gain liquidation fees. Liquidation fees depend on the type of collateral involved.

Borrow fees: interest paid to make a leveraged position. The hourly borrowing fee will vary based on utilization, equal to (assets borrowed)/(total assets in the pool)*0.01%.

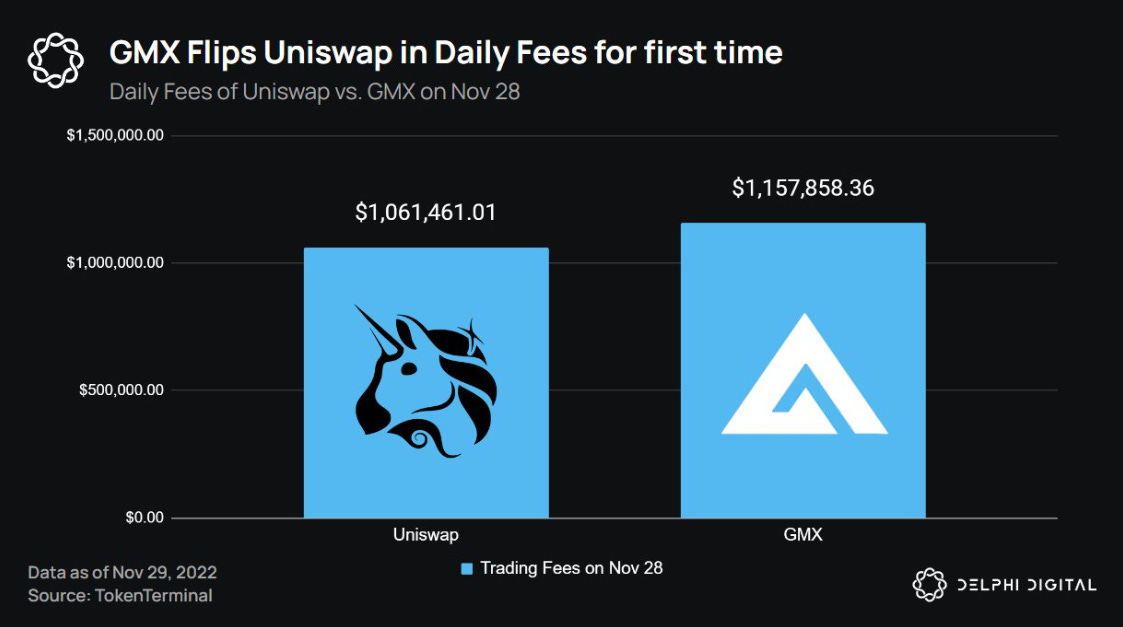

Since all generated platform fees are distributed among token holders/stakers (30% to staked GMX/esGMX holders, 70% to GLP holders), more protocol revenues increase the token holders’ value. Such design is a huge demand driver given that, right now, GMX is so appealing that the platform’s trading fees have overcome Uniswap’s:

a. Governance model

Another utility driver for token holders comes from the governance model. The core team manages GMX and maintains control over the protocol, but token holders can make suggestions and vote on proposals. Below is the high-level governance process on GMX:

Off-chain preliminary discussion

Anyone can share a proposal idea with the team on the GMX Governance Forum, and there are no requirements to discuss suggestions before putting them to a vote. An idea that grows in support by the community can be set to a governance vote by the core team.

On-chain voting

GMX token holders can vote on proposals using the GMX Snapshot Page. Voting power is calculated through an aggregation strategy of sbfGMX (Staked + Bonus + Fee GMX) and vGMX (vested $GMX).

Implementation

The GMX core team executes successful proposals which have achieved the majority quorum among token holders.

The token $GMX is supposed to be held since it guarantees owners some governance rights. Furthermore, the overall staking mechanism is a huge incentive for token holders to earn passive yield.

6. Final thoughts

Although GMX is not the first mover offering such a product, over time, it has outclassed the competition and climbed the TVL ranking, overcoming dYdX. GMX provides traders and investors with a well-developed platform to perform various financial activities like investing, trading, and passive earning. Being built on low-fee blockchains and Layer-2 solutions allow cryptocurrency investors to rotate their assets and pay pocket-friendly fees. Furthermore, GMX is one of the few platforms to offer perpetual swaps with up to 30x leverage.

As a result, it is the leading player in the crypto derivatives field whose market is far more significant than the spot's; this guarantees a consistent demand over time from users unless new relevant players occur.

As a DAO is far from true decentralization, it planned its roadmap through an internal governance process. The vision of GMX is to become an even more complete and user-friendly DEX for on-chain leverage trading. The current roadmap includes many improvements, such as:

Better UI and UX to improve traders' experience

Synthetic assets will be available on the platform

Network expansion alongside Arbitrum and Avalanche

GMX has a solid and active community which could lead to long-term sustainability since they can help to promote the token and drive adoption:

Do the incentives create common wealth, and are they value-aligned?

Absolutely yes.

Governance rights are desirable by token holders since they can take advantage of protocol decisions which may lead to higher revenues. All stakers receive fee revenues, so a considerable incentive mechanism exists to lock their tokens. Part of the revenues are allocated in $ETH/$AVAX (this relieves $GMX emission), and the $GLP mint/burn mechanism connotes a non-inflationary tokenomics model. Finally, the referral program is the extra boost a DEX needs besides that low fee, minimal liquidation risk, and capital efficiency.

a. Risks

To fully evaluate the project, we should highlight some of the associated risks:

Smart contract risks. Caution should be exercised when interacting with any smart contract or blockchain application. While testing, audits, and bug bounties attempt to mitigate risks, there is always the possibility of vulnerabilities in smart contract code.

Counterparty risks. The GLP pool is the counterparty to traders if traders make a profit that comes from the value of the GLP pool.

If profit traders » profit liquidity providers, the GLP pool could suffer low liquidity, so the protocol should allow more yield to be attractive for LPs. Often, more yield means more token inflation at the end, even though GMX token mechanism leads to controlled inflation.

Market manipulation. The token is highly volatile, and the price action looks like a spiky chart. For example, in September, a DeFi trader manipulated $AVAX by taking advantage of the difference in slippage among GMX and CEXs. Although GMX worked as designed, the team decided to cap at $2M AVAX open interest on their exchange.

Centralization risk. Per the current configuration, the keepers — some team members who choose assets’ price GMX — have some degree to charge an extra invisible price to the user. A poor initiative only sets a spread if the keeper’s price deviates from the ChainLink price by more than 2.5%. This means that a keeper can charge up to this spread value. And this would only make the price worse for the traders (non-value-aligned).

For the GMX growth, it is necessary to scale up and offer more and more assets in the platform over time. However, this could be limited and lead to a Scalability issue since high-volatile crypto assets (the majority) don’t have enough liquidity and can be manipulated.

[Systemic risk] If some events occur, like big crypto players’ insolvency, this could lead to a massive general token withdrawal which would drain liquidity pools.

b. Ideas for improvement

We can imagine some improvements to capture even more value:

Market manipulation has already occurred regarding GMX. The platform needs to enhance its security framework (even if the team argued on that occasion the protocol worked as designed). This could involve implementing cutting-edge security measures, such as advanced encryption and multi-factor authentication, to protect against hacking and other security threats.

Following the GMX roadmap to extend available assets within the platform, such as synthetics (the team must exert caution in order not to fall inside the boundary of the securities framework), more and more asset types could be game-changing for the protocol. It could include adding new cryptocurrencies and other assets, such as stocks, commodities, or even fiat currencies. Remember that offering high-volatile and low-liquid assets can result in the risk of market manipulation. In turn, it could be dangerous to accept altcoins with low-volume trades.

Building partnerships. Establishing solid relationships with other companies and organizations in the blockchain space can help to grow the platform and establish it as a trusted and respected player in the industry. This could involve partnering with other exchanges, wallet providers, or regulatory bodies.

[General crypto market concern] Regulation framework: guaranteeing regular audits by third-party companies and obtaining consumer protection certificates granted by regulatory bodies is fundamental to attracting more and more users who ask for assurance regarding their investments.

Decentralization improvement: given that the protocol is far from true decentralization, several improvements should be made to increase DAO power at the team's expense. In such a context, good decision-makers inside the DAO should be rewarded, while the bad ones should be slashed. SourceCred, for example, is a tool that allows DAOs to measure and automatically reward value creation inside the organization.

Offering even more distinct CEX products is vital to sustaining user demand. Therefore, the protocol should expand the available services to the user base to gain more competitive advantage. Some examples are options/futures with expiration dates (not only perpetual trading), loans, and institutional services (such as OTC).

Thank you for having read my article. If you like it, please follow me on my social pages and tell me how I can improve my content. I’ll be glad to consider your ideas while writing the next one.

ETH wallet for donations: 0x74151366103F899d6FD4200806eC9E9Ee588b5bD

GMX official site: https://gmx.io/#/

CoinMarketCap profile: https://coinmarketcap.com/currencies/gmx/

CoinGecko tokenomics data: https://www.coingecko.com/en/coins/gmx/tokenomics

Messari report: https://messari.io/asset/gmx

GMX analytics: https://www.gmxstats.com/

GMX trading leaderboard: https://www.gmx.house/

GMX snapshot page: https://snapshot.org/#/gmx.eth

GMX governance forum: https://gov.gmx.io/t/re-enable-shorting-for-link-and-uni/212

GMX dashboard: https://app.gmx.io/#/dashboard

GMX earn: https://app.gmx.io/#/earn

GMX gitbook page: https://gmxio.gitbook.io/gmx/

GMX technical overview: https://gmx-io.notion.site/gmx-io/GMX-Technical-Overview-47fc5ed832e243afb9e97e8a4a036353

$GMX token address (Arbitrum): https://arbiscan.io/token/0xfc5A1A6EB076a2C7aD06eD22C90d7E710E35ad0a

$GMX token address (Avalanche): https://snowtrace.io/address/0x62edc0692BD897D2295872a9FFCac5425011c661

Staked $GLP token address (Arbitrum): https://arbiscan.io/token/0x1aDDD80E6039594eE970E5872D247bf0414C8903

Staked $GLP token address (Avalanche): https://snowtrace.io/address/0x9e295B5B976a184B14aD8cd72413aD846C299660

$GMX-$WETH Uniswap liquidity pool: https://arbiscan.io/address/0x80A9ae39310abf666A87C743d6ebBD0E8C42158E

Footprint - Protocols comparison: https://www.footprint.network/@VnFApI5hnG/DEX-Perpetual-Markets-dYdX-GMX-comparison

Nanoly (ex. Coindix) - DeFi aggregator (APY): https://nanoly.com/arbitrum-ethereum-name:GMX

Optimizing token distribution: https://lstephanian.mirror.xyz/kB9Jz_5joqbY0ePO8rU1NNDKhiqvzU6OWyYsbSA-Kcc

DeFiLlama: https://defillama.com/protocol/gmx

CryptoFees: https://cryptofees.info/

Staking rewards: https://www.stakingrewards.com/earn/gmx/

Chainlist (add new chain/network to a wallet): https://chainlist.org

Further tokenomics resources: https://fstrauf.github.io/tokenomicsDAO/basic_resources/